🤑Mamma Mia! Here She Goes Again 🤑

Hi friends!

Welcome to Better Have My Money, my Monday night newsletter about stocks for people who feel out of their depth when it comes to the stock market. Better Have My Money is a gif-filled rundown about the wild world of stocks (from why we should care about shares when the world is burning, to figuring out which public companies are run by women, and picking cheapish stocks to buy).

This week I've been delving into some nerd reading about stocks, because I'm trying to get a better historical understanding of the market and how it works and what it does and how we all become filthy rich off it like generations of white men before us.

Also because ignoring history dooms you to repeat it. Today I'm going to offer you two things I've read that are less about practical tips for stocks and more like ~stocks philosophies~ which hopefully aren't as terrible as that term.

So first up, a dear friend bought me The Intelligent Investor, by Benjamin Graham, for my birthday. Cause that's the kind of cool crazy gal I've become.

Warren Buffett, aka everyone's fave investor to quote, called it "by far the best book on investing ever written." The book was originally written in the 1970s and definitely not for readers who usually prefer contemporary multi-generational immigrant fiction entwined with tales of female friendship, so some of it is a little... dull but I'm enjoying dipping into it and the updated commentary, written by Wall Street reporter Jason Zweig, is great.

Zweig wrote this bit that I keep thinking about:

Would you willing allow a certifiable lunatic to come by at least five times a week to tell you that you should feel exactly the way he feels? Would you ever agree to be euphoric just because he is — or miserable just because he thinks you should be? Of course not. You'd insist on your right to take control of your own emotional life, based on your experiences and beliefs. But when it comes to their financial lives, millions of people let Mr. Market tell them how to feel and what to do — despite the obvious fact that, from time to time, he can get nuttier than a fruitcake.... The intelligent investor shouldn't ignore Mr. Market entirely. Instead, you should do business with him — but only to the extent that it serves your interests. Mr Market's job is to provide you with prices; your job is to decide whether it is to your advantage to act on them. You do not have to trade with him just because he constantly begs you to.

OK so I love thinking of Mr. Market like some annoying dude that is begging you to hang out with him, because that also makes it easier leave him on read 'cause you felt like it etc.

I think it also helps people who feel like they can only buy stocks if they are paying attention to the market every day, reading everything, make sure they are buying at the BEST time, being super into the business or whatever. When actually, you should just serve your own interests.

Want long-term growth? Don't stress about Netflix or Facebook or Twitter being down for a few weeks because if you aren't going to sell them for years anyway, then why does it matter what happened this week? You can just ignore his texts for a bit OK!!!!!

But maybe do worry about which social media platforms encourage white supremacists! And which company kicks them off first! And this week I'd suggest giving some money to the Heather Heyer Foundation, which was set up to honor Heather who was killed one year ago this weekend in Charlottesville protesting against white supremacists. The foundation, run by her mother, is raising money for a scholarship fund for those who want to study social justice and education.

The other nerdy stocks piece I found fascinating and wanted to share is all about the psychology and behavior of investing, by Morgan Housel on Collaborative Fund (I first saw this in a newsletter from Howard Lindzon) and... it sort of made me realize why I like stocks:

In what other field does someone with no education, no relevant experience, no resources, and no connections vastly outperform someone with the best education, the most relevant experiences, the best resources and the best connections? There will never be a story of a Grace Groner performing heart surgery better than a Harvard-trained cardiologist. Or building a faster chip than Apple’s engineers. Unthinkable.

But these stories happen in investing.

That’s because investing is not the study of finance. It’s the study of how people behave with money. And behavior is hard to teach, even to really smart people. You can’t sum up behavior with formulas to memorize or spreadsheet models to follow. Behavior is inborn, varies by person, is hard to measure, changes over time, and people are prone to deny its existence, especially when describing themselves."

And the article, which goes through a bunch of different behaviors, also had this glorious tidbit about compound interest:

There are over 2,000 books picking apart how Warren Buffett built his fortune. But none are called “This Guy Has Been Investing Consistently for Three-Quarters of a Century.” But we know that’s the key to the majority of his success; it’s just hard to wrap your head around that math because it’s not intuitive. There are books on economic cycles, trading strategies, and sector bets. But the most powerful and important book should be called “Shut Up And Wait.” It’s just one page with a long-term chart of economic growth. Physicist Albert Bartlett put it: “The greatest shortcoming of the human race is our inability to understand the exponential function.”

Confusing term of the week: "compound interest" — basically, it's interest on interest aka the true key to all wealth. So it's not just that your stocks rise, say, 8%. It's that this year you earn 8% and then you next year maybe you earn 7% on your stocks which are already 8% up and then the next year you're up 9% and that's on top of the two years (the 8% and the 7%) beforehand.

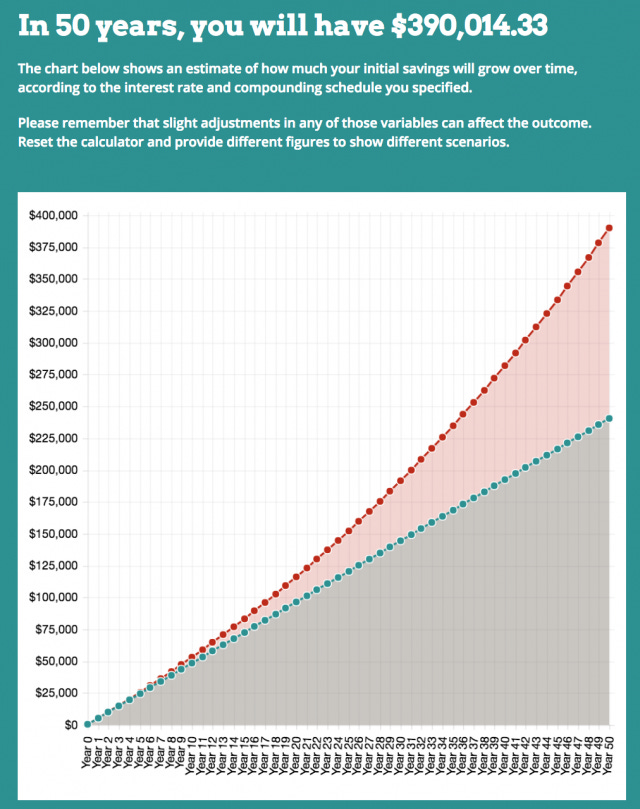

Not to get too numbery, but right now I chuck $400 every two weeks into my rainy day savings account. If I kept doing that, for the next 50 years, earning my current bank account rate of 1.8% per year, I'd end up with $390k.

If I didn't have that delicious interest compounding every year, I'd have just $240k. Here's a graph I made using this cool government approved compound interest calculator, you should also use it and see how rich you'll get over time even if you just put in a small amount every month.

I've decided not to include my own stock portfolio in this week's Better Have My Money because I think it becomes then it focuses on the week to week fluctuations which I specifically try to discourage. So I'm gonna do it once a month instead!

People keep asking me what app I use for buying stocks, which means it's been a while since I posted my regular reminder that if you open a Robinhood account, which lets you buy and sell stocks with zero fees, use my referral code and we both get a free share.

Testimonials:

Khrista via email: "I love your newsletter so much - I’ve even emailed the Netflix episode to my dad who is an investor because of me. I think the gifs confused him though ... 😹" — hi to your dad! The gifs confuse my mum too...

Any questions you're too embarrassed to ask people about stocks?

Just email me and I'll find the answer for you, shame free.

Better Have My Money is on Twitter @bhavemymoney, follow and tag us. Which of your friends would not be confused by the gifs? Forward this email to them and demand they subscribe

Also my hot tip for the week is to go see Mamma Mia! Here We Go Again, you will invest in much joy and your laughter will compound until near hysterics and you can still use MoviePass for it so it feels like a fun gamble even though you're just using a product you've paid for!